When you’ve been injured in a car accident, you have the right to be compensated for all your various damages by those responsible. This ranges from medical bills, lost wages, repairs, and compensation for your pain and suffering. But the car accident claims process can be complex, and many are left wondering how they will be paid.

Knowing what to expect throughout the car accident settlement process can help you avoid any surprises and maximize value.

After an accident, you’ll be busy trying to recover and looking to repair or replace your vehicle. Holding the at-fault party responsible is a good way to gain firm financial footing after a crash you didn’t cause, so you should understand the claims process.

Once your settlement is approved, you should receive payment.

When considering how are personal injury settlements paid, there are multiple ways you could receive your insurance settlement check. Depending on your situation, you could opt for a structured schedule of payments or a one-time lump sum payment. Fortunately, you will not have to pay taxes on your injury settlement in either case.

Many injury victims quickly decide to go for a lump sum payment. These are generally paid out within six weeks of the signed agreement, though you could expect the process to take several months. Once you receive your money, you can use it as you see fit, you’ll be able to manage your investments, and you can use the funds for immediate, unexpected expenses.

However, a lump sum payment means you’ll have to be selective with your money. If you lose money or misspend it, it’s gone.

A structured settlement may amount to receiving the same amount as a lump sum, with several payments over an extended period. Structured settlements can be annuities purchased from the insurance company by the defendant, U.S. Treasury bonds, or self-funded by the defendant.

These installments guarantee you’ll receive money for your expenses for a long time, so you’ll have continuous support. You are also protected from risky investments because you cannot access most of the settlement. However, unexpected bills may pose a risk because you can’t access those funds.

You’ll be able to discuss the best method to receive your settlement with a car accident lawyer.

The question of how are personal injury settlements paid involves more than just the total amount; you also need to consider deductions. There will be expenses deducted from the total settlement amount and other debts to consider.

You’ll need to sign a release form with your attorney, the insurance company, the liable party, and any other relevant entities to get your financial car accident settlement. This form releases the insurance company and at-fault party from any future responsibility and prohibits you from seeking more compensation for the incident that injured you in the future.

The check should be made out to you and your attorney. Once the check has been received, it can be designated into the appropriate legal trust account.

After a car accident, victims often face piling debts and expenses. Many are left to use their own money while waiting for a settlement to be reached.

Typical debts include medical bills, car rental fees, insurance co-pays, things not covered by insurance, private health insurance carrier liens, outstanding utility bills or rent, and other costs you couldn’t cover because of your injuries.

Your attorney can work on reducing some of those debts before your settlement amount gets distributed to them, and some of the accrued debts can be covered once you receive the check.

One thing to remember: your attorney will also be working for a paycheck. Most personal injury attorneys operate with a contingency fee, a “no-win, no-fee” flat rate taken out of the final settlement amount. This usually benefits you, ensuring your attorney will do their best to get you the maximum settlement so that they get paid and you get your expenses covered.

Getting the money, you’re owed after a car accident can sometimes be more complicated than it should be. Insurance companies operate in a for-profit model, meaning they want to pay as little as necessary for each case. They may try to stall your case as much as possible, but you need to remain patient and cooperate as much as possible to shorten the time it takes to settle.

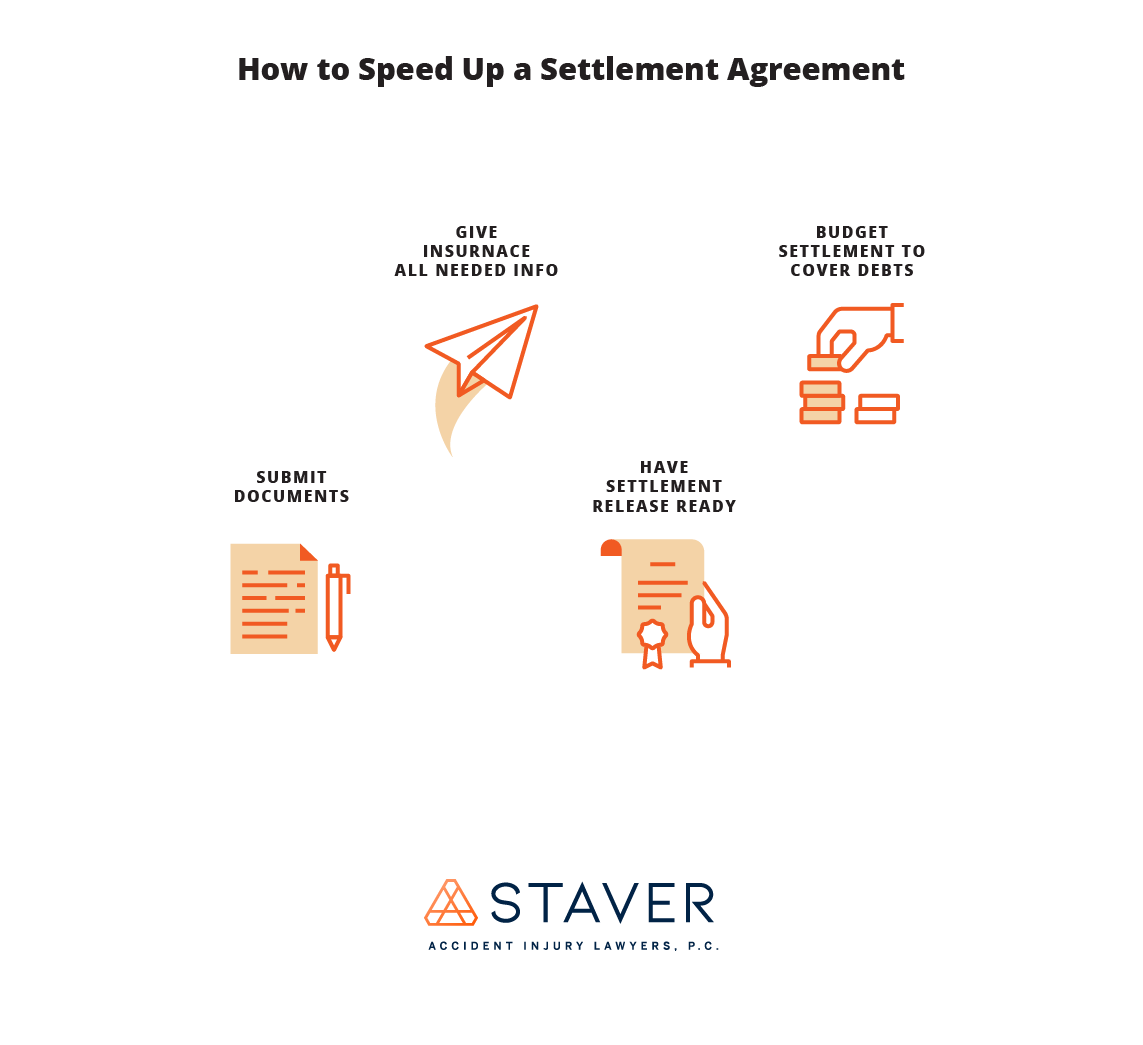

If you hope to reach a settlement agreement with your insurance company faster, you can do so by:

These are just a few examples of ways the car accident settlement check process can be hastened. If there are additional steps you can take to help recover compensation faster, your attorney should inform you accordingly.

Immediately after your car accident, you’ll want to have an attorney independently investigate the collision to establish fault. Don’t just take the insurance company’s word for what happened. Once you have established liability, you can file a claim with the liable party’s insurance company, as Illinois is a fault state for car accidents and insurance purposes.

Remember that the insurance company will look for opportunities to deny you the compensation that is rightfully yours. They may offer a lowball settlement early on, but the amount likely won’t sufficiently cover your losses. Even if you feel pressured to accept the first settlement offered, you’re well within your rights to negotiate for what you’re owed. You shouldn’t accept the initial settlement without discussing the amount with a lawyer.

Your attorney can handle the negotiations to ensure you are compensated fairly for your damages. A car accident lawyer will ensure the insurance company cuts your settlement check promptly so you can access the funds you need to cover your debts and rebuild your life.

If you have additional questions regarding your car accident settlement check, how much your case is worth, or what to expect from your car accident claim, contact our trusted Chicago personal injury lawyers at Staver Accident Injury Lawyers, P.C.

Schedule your no-cost, risk-free consultation when you call our office (312-236-2900) or complete our online contact form to get started on your case today.

When you’re fighting for maximum compensation, we know what it takes to get it.